Mit ETFs die finanzielle Gelassenheit im Alter vorbereiten und Beiträge von der Steuer absetzen

Mit diesem individuellen ETF-Portfolio für die Altersvorsorge wählen Sie aus über 200 ETFs und Indexfonds aus. Sie legen Ihr Geld zu günstigen Kosten von pauschal 36 € jährlich sowie 0,4 % p. a. an. Ihre Beiträge zahlen Sie über flexible Einzahlungen oder per Sparplan ein. Bis zu einem Höchstsatz von 27.566 € setzen Sie jährlich Ihre Beiträge zu 100 % von der Steuer ab.

Bitte beachten Sie unsere Risikohinweise.

Über 25.000 € von der Steuer absetzen

Mit dem ETF Rürup können Sie Ihre Beiträge jedes Jahr als Vorsorgeaufwendungen steuerlich absetzen. Das geht 2024 sogar bis zu 100 %.

In 2024 können Sie Ihre Rürup-Beiträge bis zu 27.566 € von der Steuer absetzen.

Für Ehegatten verdoppelt sich der abzugsfähige Betrag auf bis zu 55.131 €.

In der Auszahlungsphase wird Ihre Rürup-Rente mit Ihrem persönlichen Einkommensteuersatz versteuert.

Für wen kann sich ein ETF Rürup-Fondssparplan lohnen?

Existenzgründer und Selbstständige

Die Rürup-Rente oder "Basisrente" ist eine Möglichkeit, von einer steuerlich geförderten Altersvorsorge zu profitieren.

Topverdiener

Als Topverdiener müssen Sie mit einer besonders großen Versorgungslücke im Alter rechnen – und diese idealerweise steuerbegünstigt schließen.

Angestellte und Beamte

Mit der Rürup-Rente können Sie Ihre private Altersvorsorge ergänzen und die Beiträge von der Steuer absetzen.

Die Rürup-Förderung auf die günstigste und flexibelste Weise nutzen

Mit einem ETF-Fondssparplan für die Rürup-Rente bieten wir hohe Renditechancen bei geringen Kosten, da Ihre Erträge bis zum Rentenbeginn nicht besteuert werden. Sie bestimmen außerdem selbst über den Aufbau Ihres flexiblen Vorsorgeportfolios. Mit unserem Fondsmixer können Sie Ihre Auswahl jederzeit anpassen. Alle wählbaren Fonds finden Sie in der Fondsübersicht. Automatisiertes Rebalancing mit fünf frei wählbaren Rhythmen ist in den Leistungen inbegriffen.

Mit dem ETF Rürup in die finanzielle Gelassenheit

Mit dem ETF Rürup haben Sie Ihr Geld fest auf der hohen Kante – auf einem Konto, auf das Sie flexibel einzahlen können und keine dauerhaften Beiträge leisten müssen.

ETFs und Aktienquote können im ETF Rürup frei gewählt werden. Dies ist möglich, da auf eine Kapitalgarantie verzichtet wird, was sich positiv auf die langfristig zu erwartende Rendite auswirken kann.

Anschließend folgt zu Ihrem Rentenbeginn eine lebenslange Leibrente mit garantierten Rentenfaktoren.

Erstattung der Wechselkosten: Gesetzlich können Rürup-Verträge nicht gekündigt werden. Sie können den ETF Rürup beitragsfrei stellen und kostenlos mit dem gebildeten Vertragswert zu einem anderen Rürup-Anbieter wechseln. Wenn Sie zum ETF Rürup von Raisin wechseln, erstatten wir Ihnen die Wechselgebühren bis zu einer Höhe von 150 €.

Brauchen Sie noch Details zum ETF Rürup?

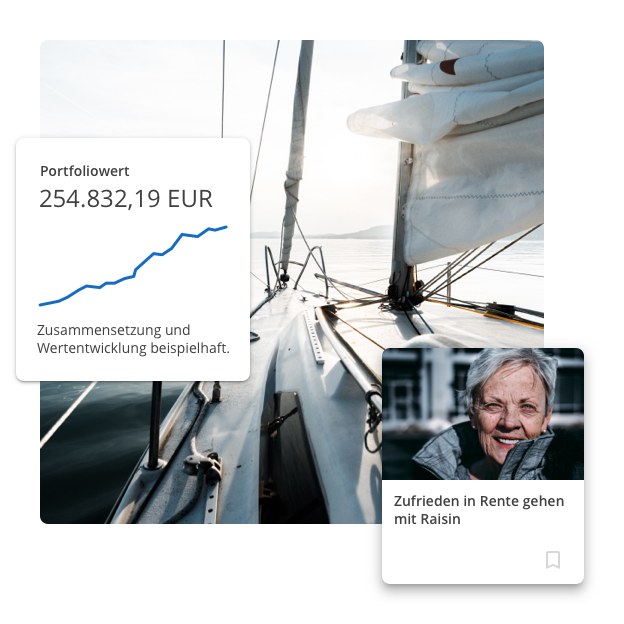

Renditechancen eines ETF Portfolios mit Steuervorteilen kombinieren

Nutzen Sie Rürup-Steuervorteile mit unserem von Finanztip ausgezeichneten ETF Rürup Fondssparplan – mit der Performance eines normalen Depots. Bitte beachten Sie, dass das Portfolio Wertschwankungen unterliegt.

Weitere Informationen finden Sie in unserem Muster-Produktinformationsblatt.